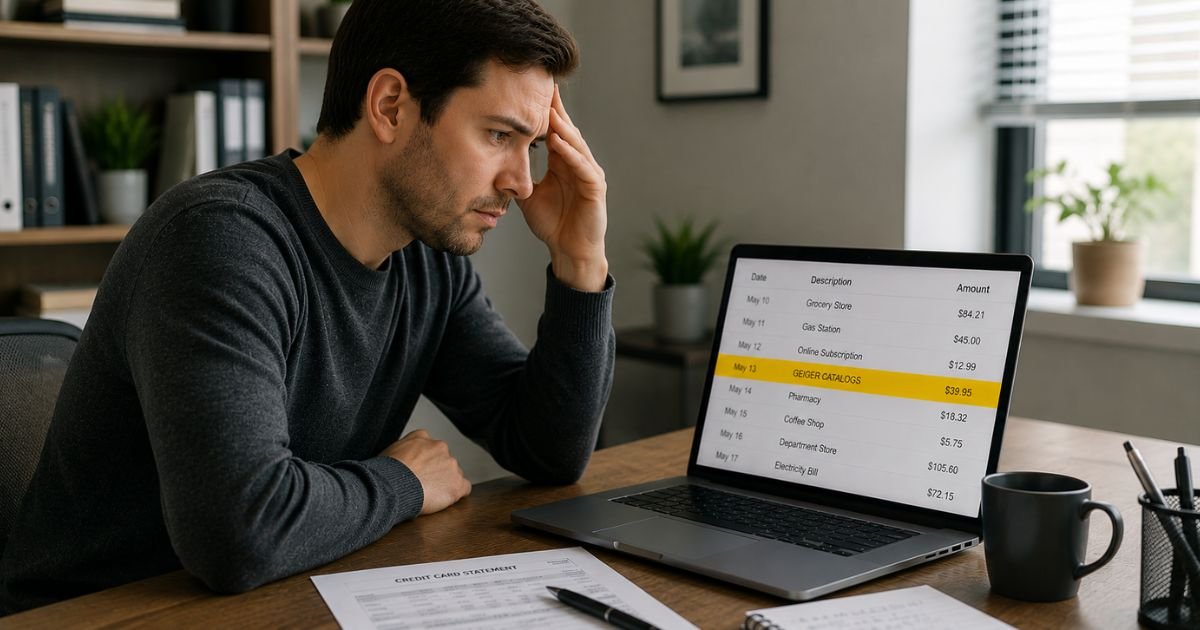

You check your credit card statement and notice a charge from Geiger, GEIGER CATALOGS, or a similar name. You don’t immediately recognize the merchant, and now you’re wondering if the charge is legitimate.

This is a common situation. “Geiger” can refer to more than one company, and the shortened billing descriptor often leaves people confused.

This article explains the most likely sources of a Geiger charge on your credit card and gives you clear steps to identify, confirm, or dispute it.

Quick Answer

A Geiger charge on credit card most often comes from Geiger (geiger.com), a major promotional products and catalog company that frequently bills as “GEIGER CATALOGS.” It can also come from Kurt Geiger, a fashion brand.

These are legitimate companies. Match the date and amount to any recent catalog order, promotional merchandise, or fashion purchase. If you still don’t recognize the charge, contact the merchant or your card issuer right away.

What Is a Geiger Charge on Credit Card?

“Geiger” or “GEIGER CATALOGS” is a billing descriptor used by Geiger, a long-established promotional products company (formerly Geiger Bros).

They sell customized branded merchandise, catalogs, and corporate gifts. Many businesses and individuals order from them, and the charge appears on statements as GEIGER CATALOGS or a close variation.

A second common possibility is Kurt Geiger, a fashion and accessories brand (shoes, bags, etc.). Their charges may appear simply as GEIGER or KURT GEIGER depending on the bank.

Because credit-card networks limit the length of merchant names, the full brand is often shortened, which causes the confusion.

Why Might You See a Geiger Charge?

Common legitimate reasons include:

- You (or your company) ordered promotional products, branded merchandise, or items from a Geiger catalog.

- You purchased shoes, bags, or fashion items from Kurt Geiger.

- An authorized user or employee used the card for a business-related order.

- A gift or corporate order was placed using your card details.

In some cases the charge can also be a pre-authorization or shipping-related amount that posts later.

Is the Geiger Charge Legitimate?

Yes, both main companies associated with this descriptor are legitimate:

- Geiger (geiger.com) – A large, well-known promotional products supplier that has been in business for decades. Their official billing name for many transactions is “GEIGER CATALOGS.”

- Kurt Geiger – A recognized fashion retailer.

The charge itself is almost always real. The issue for most people is simply not connecting the shortened name on the statement to the purchase they made.

How to Identify the Exact Source of Your Geiger Charge

- Look at the full transaction description, date, amount, and any phone number or location on your statement.

- Search your email (including spam) for order confirmations or shipping notices around that date that mention Geiger, Geiger Catalogs, or Kurt Geiger.

- Check recent purchases of promotional items, corporate gifts, catalogs, or fashion accessories.

- Ask coworkers, family members, or authorized users if they placed an order.

- Log into any accounts you have with geiger.com or kurtgeiger.com and review order history.

Matching the date and amount to an email confirmation is usually the fastest way to confirm it.

What to Do If You Don’t Recognize the Charge

Step 1: Contact the merchant

- For Geiger / GEIGER CATALOGS: Visit geiger.com or call the customer service number associated with your order (many storefronts list 800-numbers).

- For Kurt Geiger: Use the contact options on kurtgeiger.com or their regional help center.

Provide the date, amount, and last four digits of the card and ask for the order details.

Step 2: Contact your credit card issuer

If the merchant cannot explain the charge or you believe it is unauthorized:

- Report it through your bank’s app or website as an unrecognized transaction.

- Request an investigation and provisional credit if available.

- Ask them to block future charges from this merchant descriptor if you want extra protection.

Step 3: Document everything

Save screenshots of the charge, emails, and all communication. This strengthens any dispute.

Tips to Avoid Confusion with Catalog and Fashion Charges

- Save order confirmation emails in a dedicated folder.

- Use a virtual card number for one-time catalog or online fashion purchases.

- Review statements weekly, especially after placing business or gift orders.

- Note the exact merchant name at checkout so you recognize it later.

- Keep a simple list of recent catalog or promotional product orders.

FAQs About Geiger Charge on Credit Card

Q: Is a Geiger charge a scam?

No. Geiger (promotional products) and Kurt Geiger (fashion) are legitimate companies. The shortened billing name is the main reason the charge looks unfamiliar.

Q: Why does it say “GEIGER CATALOGS”?

That is the official billing descriptor used by Geiger for many of their catalog and promotional product transactions.

Q: Can I get a refund?

Yes, if the order is recent, was not received, or was unauthorized. Start with the merchant. If that fails, dispute the charge with your card issuer within the allowed time frame (usually 60–120 days).

Q: Will disputing this charge hurt my credit score?

No. A legitimate dispute for an unrecognized or unauthorized charge does not affect your credit score.

Conclusion

A Geiger charge on credit card most often comes from Geiger (billing as GEIGER CATALOGS), a major promotional products company, or from Kurt Geiger fashion purchases. Both are legitimate.

Match the date and amount to any recent catalog, promotional, or fashion order. If you still do not recognize the charge, contact the merchant first and then your credit card issuer to investigate or dispute it.

Taking these steps quickly protects your account and resolves the mystery.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or professional advice. Billing descriptors and company practices can change. Always verify details with the merchant listed on your statement and your credit card issuer. For personalized help, contact your bank or a consumer protection agency such as the CFPB.