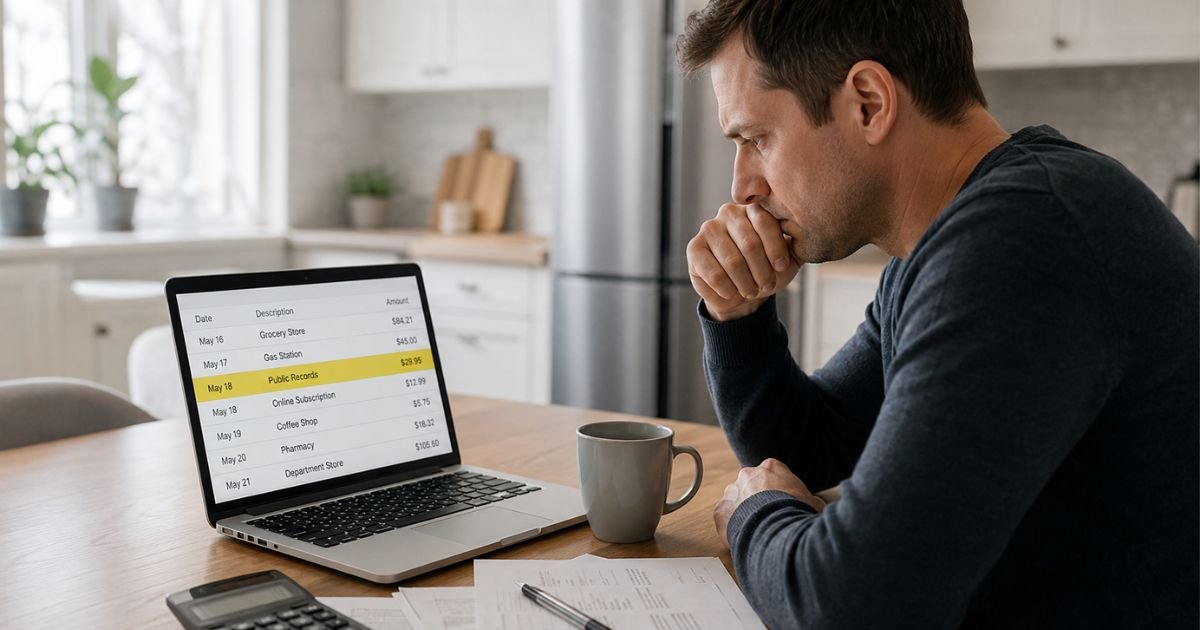

You open your credit card statement and notice a charge labeled “Public Records,” “PublicRecords.info,” or something similar that you don’t recognize.

Your first thought is probably fraud or a mistake. You’re not alone. Thousands of people every month search for answers about unexpected public records charges on their credit cards.

These charges almost always come from legitimate (though often poorly disclosed) subscription services that aggregate public records.

This article explains exactly where the charges come from, why they recur, and the precise steps you can take today to stop them and potentially get your money back.

Quick Answer

A public records charge on credit card usually means you (or someone using your card) signed up for a subscription service that provides easy access to compiled public records such as court documents, property records, addresses, and relatives.

Most of these services start with a low one-time or trial fee, then automatically convert to recurring monthly or annual billing. If the charge is unfamiliar, it is often the result of unclear terms during signup rather than outright fraud.

What Does a Public Records Charge on Credit Card Actually Mean?

These charges appear when you purchase access to online databases that pull together publicly available information from government sources. The companies are not credit reporting agencies and do not sell official documents.

They simply make searching multiple county, state, and federal records faster and more convenient than visiting individual government websites.

The billing descriptor on your statement is often shortened. You might see:

- PublicRecords.info

- Public Record Reports

- PublicRecords.us

- CourtRecords.us

- SearchPublicRecords.com

- Or simply “PUBLIC RECORDS”

These are the merchant names these companies use with their payment processors.

Why Do Public Records Charges Keep Appearing Every Month?

Most complaints involve recurring billing that customers did not expect. Here’s how it typically happens:

- You pay a small fee (often $1 or $9.95) for a single report or trial.

- The fine print states that your card will be charged the full subscription price (commonly $19.95–$29.95 per month or higher annual amounts) unless you cancel before the trial ends.

- Many people miss the cancellation window or do not realize a subscription was created.

- Some services make cancellation more difficult than signup by requiring phone calls or specific account logins.

Consumer reviews on Trustpilot and ConsumerAffairs frequently mention surprise charges that continue for months before the cardholder notices.

Is This a Scam or a Legitimate Charge?

These are real companies providing a real (if limited) service. They compile public records that anyone can access for free through government portals, but they charge for convenience and speed. The service itself is legal.

However, many customers feel the billing practices are misleading. The companies themselves state clearly on their sites that they are not consumer reporting agencies and the information should not be used for credit, employment, or tenant screening decisions.

If you never signed up at all, it could be unauthorized use of your card by someone else (family member, shared computer, etc.). In that case, treat it as potential fraud.

How to Identify the Exact Company Behind the Charge

- Look at the full transaction description on your statement or online banking app. It often includes a phone number or website.

- Google the exact descriptor plus the word “charge” or “cancel.”

- Check your email (including spam) for any confirmation messages around the date of the first charge.

- Log into any recent accounts you created for background checks, people searches, or property records.

Common support contacts include:

- PublicRecords.info: 1-877-381-8701 or support@publicrecords.info

- PublicRecords.us: 1-888-700-8184

How to Cancel a Public Records Subscription

Follow these steps in order:

- Visit the website mentioned in the charge or search for it directly. Create or log into an account using the email tied to the charge.

- Look for “Account Settings,” “Subscription,” “Billing,” or “My Account.”

- Find and select the option to cancel subscription or close the account. Many sites have a “Close Account” button at the bottom of the page.

- Call customer support if the website option is unclear. Have your account email and last four digits of the card ready. Ask for written confirmation of cancellation.

- Request a refund for recent charges while on the phone. Some representatives issue refunds as a courtesy, especially for first-time issues.

- Save all emails and chat transcripts.

If you cannot find the website, contact your credit card issuer. They can often provide the merchant’s phone number or help initiate a dispute.

How to Dispute the Charge with Your Credit Card Company

If the company will not refund you or you believe the charge was unauthorized:

- Log into your credit card account and open a dispute for the specific transaction.

- Select reasons such as “Recurring billing not authorized” or “Services not as described.”

- Provide any evidence you have (no confirmation email, cancellation attempts, etc.).

- Most issuers give you provisional credit while they investigate.

- You generally have 60–120 days from the statement date to dispute, but act quickly.

For recurring charges, you can also ask your bank to block future charges from that merchant.

Tips to Avoid Surprise Subscription Charges Going Forward

- Use a virtual card number or privacy-focused card (such as those from Privacy.com) for any trial offers.

- Set a phone reminder or calendar event for the exact day a trial ends.

- Read the full terms and look for phrases like “automatically renews” or “subscription” before entering payment information.

- Review your credit card statements and email confirmations within 48 hours of any new signup.

- Keep a simple note in your password manager with the date and company name whenever you enter card details.

Are Public Records Search Services Actually Useful?

These services can save time when you need to find old addresses, relatives, property ownership history, or court records across multiple jurisdictions.

However, the same information is usually available for free (though slower) through county clerk websites, state court portals, and sites like PACER for federal records.

Use them only when you need quick, consolidated results and understand exactly what you are paying for.

FAQs About Public Records Charge on Credit Card

Q: Is a public records charge on my credit card a scam?

No, these are typically legitimate subscription services. The frustration usually comes from unclear billing practices rather than fraudulent activity. Always verify by checking recent signups and contacting the merchant directly.

Q: How much do public records subscriptions usually cost?

Introductory offers often start at $1–$10 for a single report or short trial. Recurring charges commonly range from $19.95 to $29.95 per month or higher annual fees, depending on the plan chosen at signup.

Q: Can I get a refund for past public records charges?

Many people successfully receive refunds by contacting customer support promptly, especially for the first or second charge. If the company refuses, dispute the charge with your credit card issuer and explain the circumstances.

Q: Will these charges affect my credit score?

A billing dispute itself does not hurt your credit score. However, if the charge goes to collections (rare for these amounts), it could eventually appear. Resolve the issue directly with the company or your card issuer to avoid complications.

Conclusion

A public records charge on credit card almost always traces back to a subscription for compiled public data rather than fraud or a government fee. The good news is that most of these charges can be stopped quickly by contacting the company or your card issuer.

Start today by examining the exact descriptor on your statement, searching for the company’s cancellation process, and reaching out to support.

Taking these steps protects your money and prevents ongoing charges. Stay mindful with trial offers in the future, and you can avoid this situation entirely.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or professional advice. Consumer rights, billing practices, and dispute processes can vary. Contact your credit card issuer, a consumer protection agency such as the CFPB, or a qualified professional for guidance specific to your situation. Company names, contact information, and practices mentioned are based on publicly reported consumer experiences and company websites as of 2026 and may change.